by

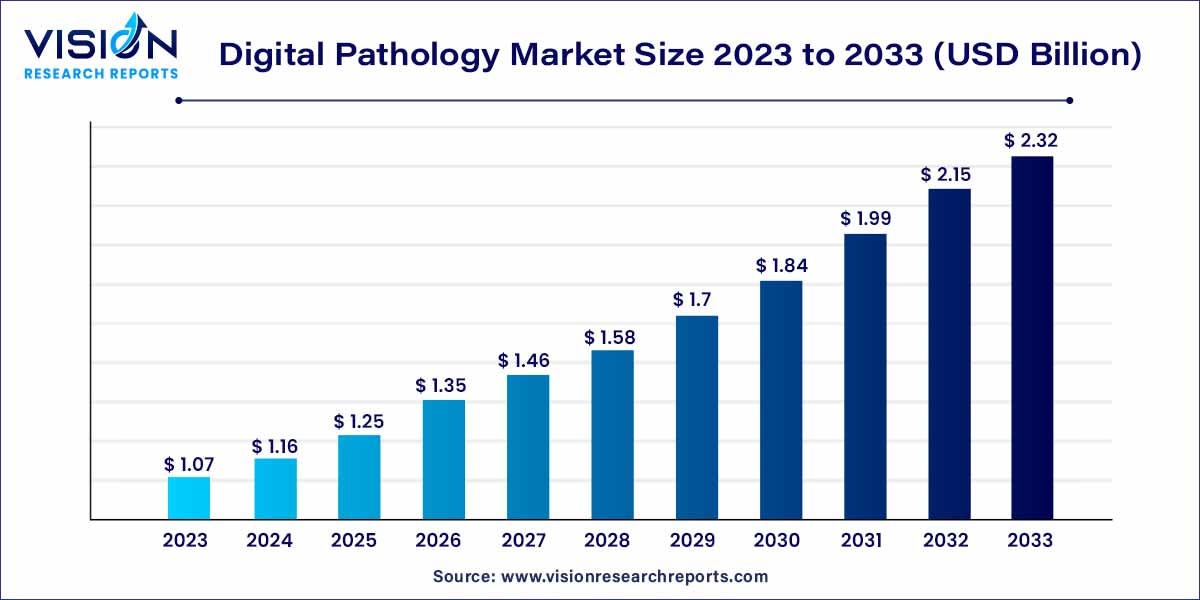

by The global digital pathology market size was estimated at around USD 1.07 billion in 2023 and it is projected to hit around USD 2.32 billion by 2033, growing at a CAGR of 8.06% from 2024 to 2033.

Key Pointers

- In 2023, North America held the biggest market share of 41%, dominating the industry.

- The fastest CAGR is expected to be seen in the Asia Pacific region between 2024 and 2033.

- In terms of product, the device category held the largest market share in 2023—52%.

- According to projections, the software industry is expected to increase at the quickest rate between 2024 and 2033.

- In 2023, the academic research category achieved the highest market share of 46% based on application.

- The application category that deals with disease diagnostics is expected to develop at the quickest rate between 2024 and 2033.

- In terms of market share by type, the human pathology sector held the highest proportion of 61% in 2023.

Digital Pathology Market Growth

The digital pathology market is undergoing robust growth, driven by several key factors. One major catalyst is the increasing adoption of digital platforms, reshaping traditional pathology practices within healthcare institutions. The incorporation of technological advancements such as whole-slide imaging, artificial intelligence (AI), and cloud-based solutions is further propelling this expansion. These innovations provide pathologists with tools that boost efficiency, streamline workflows, and contribute to enhanced diagnostic accuracy.

The rising demand for telepathology, facilitated by digital pathology, is eliminating geographical constraints, enabling remote pathology consultations, and improving access to expert opinions. As the industry experiences a greater integration of AI for pattern recognition and precise diagnostics, collaborations and partnerships between digital pathology solution providers and healthcare institutions are becoming more common. These partnerships are instrumental in driving the development of innovative and customized pathology solutions.

Digital Pathology Market Dynamics

Digital Pathology Market Drivers

- Increased Adoption of Digital Platforms: The digital pathology market is experiencing significant growth driven by the widespread adoption of digital platforms. Healthcare institutions are increasingly transitioning from traditional pathology practices to digital solutions, leading to enhanced efficiency and streamlined workflows.

- Growing Demand for Telepathology: The rising demand for telepathology services is a key driver for the digital pathology market. Enabled by digital pathology, telepathology allows for remote pathology consultations, improving accessibility to expert opinions and overcoming geographical constraints.

Digital Pathology Market Restraints

- Data Interoperability Issues: Achieving seamless data interoperability is another challenge faced by the digital pathology market. Integrating digital pathology systems with existing healthcare IT infrastructure can be complex, leading to issues related to data sharing, communication, and interoperability between different platforms.

- Workforce Training and Resistance to Change: The transition from traditional pathology practices to digital pathology requires a skilled workforce. Training pathologists and healthcare professionals to effectively use digital pathology systems can be time-consuming. Resistance to change within established practices may further impede the smooth adoption of digital pathology solutions.

Digital Pathology Market Opportunities

- Expanding Applications in Research and Drug Development: A significant opportunity for the digital pathology market lies in its expanding applications in research and drug development. Digital pathology systems provide a platform for more efficient and detailed analysis of pathology specimens, facilitating advancements in research and aiding pharmaceutical companies in drug discovery and development processes.

- Rise of Remote Patient Consultations: The increasing adoption of telepathology opens up opportunities for remote patient consultations. Digital pathology enables pathologists to collaborate and provide expert opinions from a distance, improving patient access to specialized diagnostic services and overcoming geographical constraints.

Get a Sample: https://www.visionresearchreports.com/report/sample/41149

Product Insights

In 2023, the device segment claimed the largest market share at 52%, and this sector is expected to maintain robust growth throughout the projected period. Comprising slide management systems and scanners, this segment’s expansion is fueled by the increasing adoption of digital pathology, particularly in academic research activities where enhanced resolution capabilities are particularly advantageous.

The software segment is anticipated to exhibit the fastest growth rate from 2024 to 2033, propelled by a rising number of cancer cases. Key industry players are actively involved in the development of novel digital pathology systems, driving the demand for software solutions. For instance, Xybion Corp. introduced Pristima XD Digital Pathology in August 2021, enhancing lab throughput and streamlining workflows. Additionally, F. Hoffmann-La Roche Ltd. contributed to this trend by launching uPath enterprise software in January 2019, aimed at improving performance, speed, and overall usability in the field of digital pathology. This trend underscores the industry’s commitment to advancing technological solutions to meet evolving healthcare needs.

End-use Insights

In 2023, the device segment asserted its dominance in the market, capturing a substantial share of 52% and is positioned for lucrative growth throughout the projected period. This segment, which includes slide management systems and scanners, is witnessing a surge in demand driven by the expanding adoption of digital pathology in academic research activities. The enhanced resolution capabilities of these systems are particularly advantageous in this context. An illustrative example is the CE marking received by F. Hoffmann-La Roche Ltd. in June 2022 for its VENTANA DP 600 slide scanner. This next-generation, high-capacity scanner generates precise, high-resolution digital images of stained tissue samples, proving instrumental in cancer diagnosis and treatment planning.

Simultaneously, the software segment is expected to exhibit the fastest growth rate from 2024 to 2033. This upward trajectory is linked to the escalating number of cancer cases, prompting key industry players to focus on developing innovative digital pathology systems. For instance, in August 2021, Xybion Corp. introduced Pristima XD Digital Pathology, a solution designed to enhance lab throughput and streamline workflows. Additionally, F. Hoffmann-La Roche Ltd. contributed to this trend with the launch of uPath enterprise software in January 2019. This software is geared towards enhancing performance, speed, and usability in the realm of digital pathology. These developments highlight the industry’s commitment to advancing technology for more effective pathology solutions.

Application Insights

In 2023, the academic research segment claimed a prominent position, securing a substantial market share of 46%. This dominance is anticipated to persist from 2024 to 2033, propelled by ongoing research efforts in cancer therapy development and the widespread adoption of digital pathology in diverse research studies. Academic research institutes are actively engaging with digital pathology providers to integrate this technology into their research activities, exemplified by the noteworthy partnership between the University Medical Center Utrecht and Paige in November 2022.

The disease diagnosis segment is poised to exhibit the fastest growth rate from 2024 to 2033. This acceleration is attributed to the rising prevalence of chronic diseases and manufacturers’ increasing focus on developing rapid and innovative diagnostic techniques. These advancements aim to facilitate the seamless circulation of information within and between departments. The digital adoption of technologies plays a crucial role in enhancing the efficiency of disease diagnosis, ultimately improving therapeutic outcomes. This signifies the pivotal role of digital pathology in advancing diagnostic capabilities and contributing to more effective healthcare solutions.

Type Insights

In 2023, the human pathology segment claimed the majority share, representing approximately 61% of the market. The growth of this segment is driven by the increasing adoption of digital pathology, aimed at reducing the turnaround time for disease diagnosis and enhancing laboratory productivity. Additionally, the surge in the prevalence of chronic diseases in humans has heightened the demand for digital pathology solutions within this segment.

Forecasts indicate significant growth for veterinary digital pathology in the upcoming years. The implementation of digital pathology in the veterinary sector is facilitated by fewer restrictions on virtual scanned slides for veterinary diagnoses. Furthermore, a proactive push for automation within the veterinary field is contributing to the increased demand for digital pathology solutions, highlighting its potential impact and growth opportunities in the veterinary diagnostics domain.

Regional Insights

In 2023, North America established its dominance in the overall market, commanding a significant share of 41%. This leadership can be attributed to various factors, including increasing government initiatives promoting the development of technologically advanced pathologies, continuous investments in research and development (R&D), a growing adoption of digital imaging, and the presence of key market players focused on delivering advanced solutions. Notably, in March 2023, PathAI launched AISight, a digital pathology platform across 13 leading health systems, reference laboratories, medical centers, and independent pathology organizations in the U.S. This initiative was part of an Early Access Program aimed at providing enhanced solutions to the population. The increasing use of digital pathology in academic research and disease diagnosis further contributes to market growth in the region.

On the other hand, the Asia Pacific region is poised to exhibit the fastest Compound Annual Growth Rate (CAGR) from 2024 to 2033. This growth is driven by factors such as rapid digitalization, increased investments in the medical field, and the expanding penetration of digital imaging in developing economies. The region is experiencing a rising prevalence of cancer, necessitating novel treatment options, which, in turn, contributes to the accelerated growth of the digital pathology market. Noteworthy collaborations, such as the one in March 2023 between Qritive and Corista for the integration of artificial intelligence (AI) using DP3, a DICOM-compliant pathology software in digital pathology, showcase initiatives aimed at providing improved patient care, novel treatment options, and simultaneously reducing laboratory cost expenses.

Read More: https://www.heathcareinsights.com/molecular-diagnostics-market/

Digital Pathology Market Key Companies

- Leica Biosystems Nussloch GmbH (Danaher)

- Hamamatsu Photonics, Inc.

- Koninklijke Philips N.V.

- Olympus Corporation

- F. Hoffmann-La Roche Ltd.

- Mikroscan Technologies, Inc.

- Inspirata, Inc.

- Epredia (3DHISTECH Ltd.)

- Visiopharm A/S

- Huron Technologies International Inc.

- ContextVision AB

- CellaVision

- HANGZHOU ZHIWEI INFORMATION TECHNOLOGY CO. LTD. (MORPHOGO)

- West Medica Produktions- und Handels- GmbH (West Medica)

- aetherAI

- IBEX (IBEX MEDICAL ANALYTICS)

- SigTuple Technologies Private Limited

- Morphle Labs, Inc

- Bionovation Biotech, Inc.

Digital Pathology Market Segmentations:

By Product

- Software

- Integrated Software

- Standalone Software

- Device

- Scanners

- Brightfield Scanners

- Fluorescence Scanners

- Others

- Slide Management System

- Storage System

By Type

- Human Pathology

- Veterinary Pathology

By Application

- Drug Discovery & Development

- Academic Research

- Disease Diagnosis

- Cancer Cell Detection

- Others

By End-use

- Hospitals

- Biotech & Pharma Companies

- Diagnostic Labs

- Academic & Research Institutes

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Buy this Premium Research Report@ https://www.visionresearchreports.com/report/checkout/41149

You can place an order or ask any questions, please feel free to contact sales@visionresearchreports.com| +1 650-460-3308