by

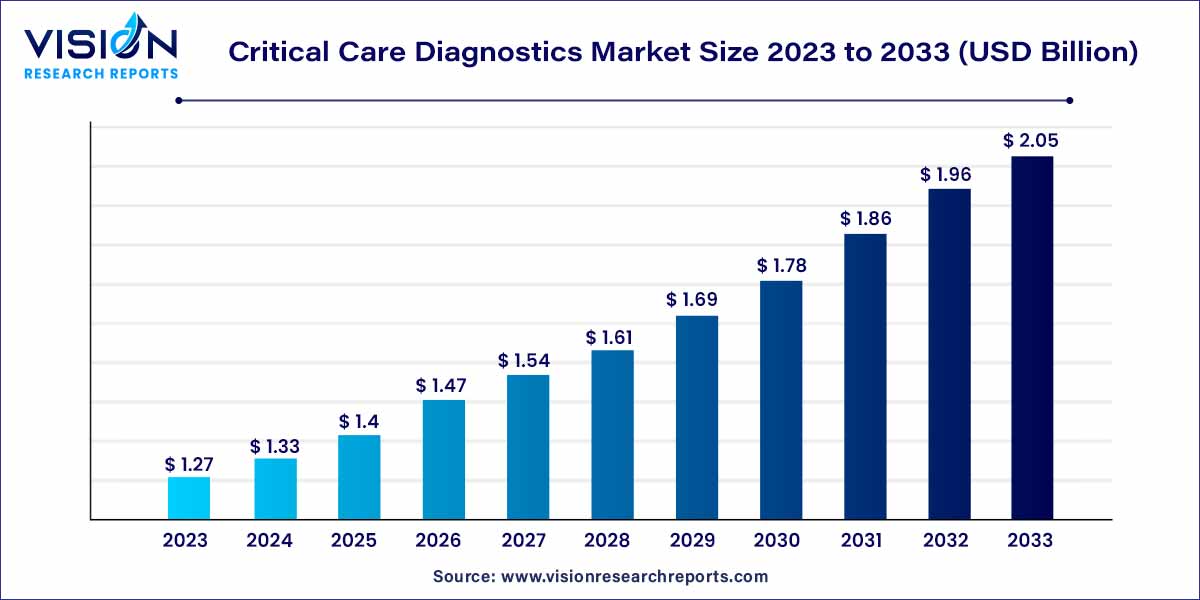

by The global critical care diagnostics market size was estimated at around USD 1.21 billion in 2022 and it is projected to hit around USD 1.96 billion by 2032, growing at a CAGR of 4.93% from 2023 to 2032. The critical care diagnostics market in the United States was accounted for USD 418.9 million in 2022.

Key Pointers

- North America led the market with the largest revenue share of 44% in 2022.

- Asia Pacific is anticipated to grow at the fastest CAGR of 6.93% over the forecast period

- By Type, the immunoproteins segment contributed the largest market share of 37% in 2022.

- By Type, the microbial and infectious disease segment is anticipated to grow at the fastest CAGR of 5.53% from 2023 to 2032.

- By End-use, the emergency rooms segment generated the maximum market share of 34% in 2022 and is also expected to grow at the fastest CAGR of 5.63% between 2023 to 2032.

The critical care diagnostics market is a dynamic sector within the broader healthcare industry, characterized by its focus on providing rapid and precise diagnostic solutions for critically ill patients. This segment has gained increasing prominence due to its pivotal role in facilitating timely and informed medical interventions.

Market Growth

The growth of the critical care diagnostics market is propelled by a confluence of factors that collectively contribute to its expanding trajectory. One significant driver is the continual evolution of diagnostic technologies, ushering in rapid and more accurate methods for assessing critically ill patients. The rising prevalence of life-threatening conditions, coupled with an increasing demand for prompt and precise diagnostic solutions, further stimulates market growth. The advent of Point-of-Care Testing (POCT) has emerged as a transformative trend, enabling healthcare professionals to conduct on-the-spot diagnostics, thereby expediting decision-making processes. Additionally, the integration of Artificial Intelligence (AI) has elevated the diagnostic landscape, fostering more nuanced and data-driven patient assessments. While the market is on an upward trajectory, challenges such as regulatory complexities and the necessity for substantial research and development investments underscore the need for strategic navigation. In navigating these challenges, the critical care diagnostics market is positioned for sustained growth, driven by a commitment to technological innovation, improved patient outcomes, and enhanced healthcare efficiency.

Get a Sample: https://www.visionresearchreports.com/report/sample/40947

Report Scope of the Critical Care Diagnostics Market

| Report Coverage | Details |

| Market Revenue by 2032 | USD 1.96 billion |

| Growth Rate from 2023 to 2032 | CAGR of 4.93% |

| Revenue Share of North America in 2022 | 44% |

| CAGR of Asia Pacific from 2023 to 2032 | 6.93% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Market Analysis (Terms Used) | Value (US$ Million/Billion) or (Volume/Units) |

Market Dynamics

Drivers

Increasing Prevalence of Critical Conditions:

The growing global burden of life-threatening conditions, such as sepsis, cardiac emergencies, and respiratory disorders, is a major driver, necessitating efficient and rapid diagnostic solutions for timely interventions.

Rise of Point-of-Care Testing (POCT):

The adoption of decentralized testing through Point-of-Care Testing (POCT) is a significant driver, allowing for on-the-spot diagnostics and quick decision-making at the patient’s bedside.

Restraints

Global Economic Uncertainties:

Economic uncertainties, both on a global scale and within specific regions, can impact healthcare budgets and investment decisions. This can, in turn, affect the funding available for the development and adoption of advanced critical care diagnostics.

Data Security Concerns:

With the increasing integration of Artificial Intelligence (AI) in diagnostics, concerns about data security and patient privacy may act as a restraint. Ensuring the secure handling of sensitive patient information is crucial for gaining trust in AI-driven diagnostic solutions.

Opportunities

Increasing Demand for Remote Patient Monitoring:

The rise in remote patient monitoring creates opportunities for innovative critical care diagnostics that can provide real-time data and facilitate timely interventions, especially in cases of chronic conditions and post-acute care.

Emergence of Advanced Biomarkers:

Ongoing research in biomarker discovery presents opportunities for the development of novel diagnostic assays, enabling more accurate and early detection of critical conditions, thereby improving patient outcomes.

Type Insights

The market is categorized into routine and special chemistry, flow cytometry, hematology, immunoproteins, microbial and infectious diseases, coagulation, and others. The immunoproteins segment dominated the market with the largest revenue share of 37% in 2022. Immunoproteins are amino acids that function in the immune system, a system of biological functions that guards an organism against disease. The immune system can detect and respond to various pathogens, such as bacteria, viruses, parasites, fungi, cancer cells, and foreign objects. Immunoproteins are involved in both the innate immune system and the adaptive immune system of the immune system, and they can be classified into different types, such as antibodies, cytokines, complement proteins, and major histocompatibility complex proteins.

The microbial and infectious disease segment is expected to grow at the fastest CAGR of 5.53% over the forecast period. These diseases are caused by microorganisms such as bacteria, viruses, parasites, and fungi. Diseases such as HIV, flu, measles, and COVID-19 are examples of microbial and infectious diseases. The segment growth is majorly driven by factors, such as clinical chemistry, flow cytometry tests, and coagulation tests, among others. Moreover, microbiology, infectious tests, and immunoproteins assays are estimated to drive segment growth over the forecast period.

The hematology segment is expected to grow at a lucrative CAGR over the forecast period owing to constant innovative and advanced product launches by market players. For instance, in May 2023, Siemens Healthcare GmbH, a medical devices company based in Germany, announced the launch of two new innovative hematology analyzers: the Atellica HEMA 580 and 570 Analyzers. The analyzers provide user-friendly interfaces and seamless connectivity to multiple analyzers, enhancing workflow efficiency and rapid throughput. These analyzers are designed to eliminate obstacles in the laboratory workflow, enabling streamlined operations and accelerated processing of samples.

End-use Insights

On the basis of end use, the market has been segmented into operation rooms, intensive care units, emergency rooms, and others. The emergency rooms segment led the market with the highest revenue share of 34% in 2022 and is also expected to grow at the fastest CAGR of 5.63% over the forecast period. This can be attributed to the prevalence of chronic diseases such as heart strokes, heart attacks, kidney failure, and a rise in mental issues such as anxiety, depression, and other disorders.

The intensive care unit segment is expected to grow at a lucrative CAGR during the forecast period owing to the increasing prevalence of chronic conditions in the U.S. According to the U.S. Department of Health & Human Services, the average ICU occupancy rate in the U.S. was 76.3% as of December 2022. This means that out of 79,271 staffed ICU beds in the country, 60,503 were occupied by patients, of which 12,345 were COVID-19 cases.

Regional Insights

North America dominated the market with the largest revenue share of 44% in 2022, owing to better healthcare infrastructure, more healthcare spending, and better technological acceptance. According to America Medical Association, the U.S. spent USD 4.3 trillion on healthcare, which equates to USD 12,194 per capita. The overall health spending was around 18.3% of the GDP in the same year.

Asia Pacific is expected to grow at the fastest CAGR of 6.93% over the forecast period due to the high patient population, rising healthcare awareness, increasing investment in healthcare, and various government initiatives. Pneumonia is one of the largest infectious diseases which causes death in children globally. According to the World Health Organization (WHO), it accounts for 14% of deaths in children under five years, killing 740,180 children in 2019. Southern Asia and sub-Saharan Africa toll for the highest number of deaths in children due to pneumonia.

The increasing prevalence of diseases such as pneumonia in the Asia Pacific countries is one of the major factors driving the demand for diagnostics in critical care settings. In addition, various healthcare organizations are undertaking strategic activities such as innovative product and service launches to gain a competitive advantage, resulting in an increasing demand for critical care diagnostics. For instance, in August 2019, Brains Super Speciality Hospital, a provider of complete care for a wide range of health conditions specializing in neurosurgery and brain care, announced the launch of advanced operating suites at BR Life SSNMC Hospital. The operation theatre complex features dedicated operating rooms equipped with state-of-the-art technology to ensure the safety and efficacy of brain and spine surgeries. This complex comprises independent operating suites designed to meet the specific requirements of these specialized procedures. The operating theatre is versatile, facilitating both micro-surgery and simultaneous cerebrovascular intervention. This dual-purpose capability provides a sophisticated operating environment and includes a compact cerebral angiography suite for precise imaging during procedures.

Key Companies

- Abbott

- Danaher

- F. Hoffmann-La Roche Ltd

- BD

- EKF Diagnostics

- bioMérieux, Inc.

- Siemens Healthcare Private Limited

- Chembio Diagnostics, Inc.

- Bayer AG

Critical Care Diagnostics Market Report Segmentations:

By Type

- Routine & Special Chemistry

- Flow Cytometry

- Hematology

- Immunoproteins

- Microbial & Infectious Disease

- Coagulation Testing

- Others

By End-use

- Operation Room

- Intensive Care Unit

- Emergency Rooms

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Buy this Premium Research Report@ https://www.visionresearchreports.com/report/checkout/40947

You can place an order or ask any questions, please feel free to contact sales@visionresearchreports.com| +1 650-460-3308