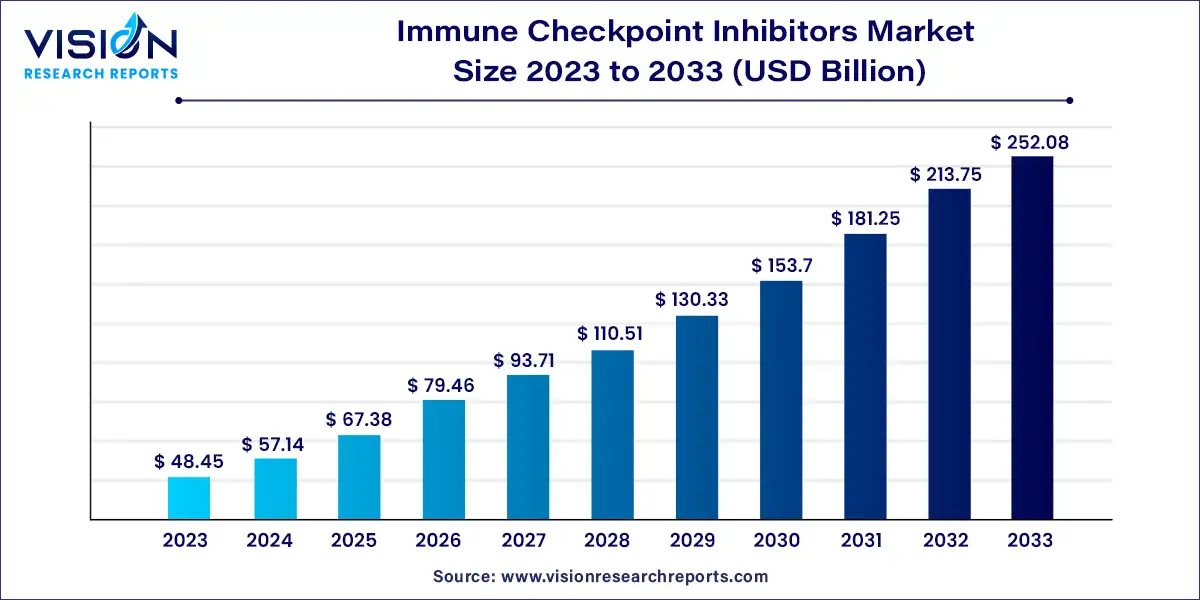

The global immune checkpoint inhibitors market size stood at USD 48.45 billion in 2023 and it is predicted to rise to USD 252.08 billion by 2033 with growing at a CAGR of 17.93% from 2024 to 2033.

The immune system’s task is to safeguard the body’s healthy cells from invasion by foreign substances (such as bacteria and cancer cells). Immunotherapy, which includes checkpoint inhibitors, is effective in treating cancers like lung and melanoma skin cancer. When immune cells with the name T cells have certain proteins on their surface, the immunological checkpoints are activated (recognizers). These checkpoints also interact with companion proteins in other cells, such as malignant cells. As a result, these cells assist in preventing the immune system from eliminating cancer.

Immune Checkpoint Inhibitors Market Highlights:

Immune Checkpoint Inhibitors Market Growth

Areas of cancer are treated with radiation and surgery, and the field of oncology is broad and includes a variety of application areas. Chemotherapy typically circulates via the bloodstream to treat patients’ entire bodies, and doing so is referred to as systemic treatment. Treatment for cancer cells helps patients’ immune systems fight cancer more successfully. The top cause of death in the world is cancer. Immune checkpoint inhibitors thereby prevent the growth of cancer cells and aid in their detection by the immune system or cells.

Immune cells that must be activated and deactivated in order to initiate an immune response and prevent the immune system from being harmed are targeted by immune checkpoint inhibitor medications. Additionally, a number of well-known companies are funding clinical development through R&D investments. The checkpoint inhibitor pembrolizumab was the first FDA-approved drug solely based on the presence of a genetic characteristic in a tumor, and it is used to treat MSI-H and dMMR cancers. Immune checkpoint inhibitors are a growing market due to ongoing rivalry in the industry.

Immune Checkpoint Inhibitors Market Regional Study

Market Dynamics of Immune Checkpoint Inhibitors Market

Market Drivers

- Immune checkpoint inhibitors are a growing market due to ongoing rivalry in the industry. The market for immune checkpoint inhibitors is expanding due to factors such as the adoption of an unhealthy lifestyle, the rise in cancer cases, and genetic mutation and alteration that have an impact on the cost of healthcare in the nation.

- In addition, rising healthcare costs in this market, an increase in the use of immune checkpoint inhibitor medications in emerging regions, and technical advancements in cancer screening and broadcasting methods are all driving the immune checkpoint inhibitors industry’s growth.

Market Restraints

- However, the high cost of product research and development subsequently raises the price of the finished product and related treatments, which is a factor that is anticipated to restrain the market growth for immune checkpoint inhibitors.

- Additionally, regulatory price limitation has resulted from the immune checkpoint medicines high price. It is also anticipated that the regulatory price cap on immune checkpoint inhibitors may impede the market’s expansion.

- The immune checkpoint inhibitors market is also being constrained by advancing cancer therapeutic technology and growing public awareness of immune system disorders.

Market Opportunities

- In order to advance their research projects, worldwide players in the immune checkpoint inhibitors market frequently collaborate with businesses that combine their core capabilities. For instance, Merck, which is known as MSD outside of the United States and Canada, and Dynavax Technologies Corporation are investigating the potential synergistic effects of combining SD-101 from Dynavax with Keytruda and MK-1966, two immunological treatments from Merck.

- A rise in the need for cancer therapies, an expansion of R&D projects, and increased reimbursement practices provided by manufacturers and insurance firms in some nations are significant drivers of the global market’s expansion.

Ask here for more customization study@ https://www.visionresearchreports.com/report/customization/39336

Immune Checkpoint Inhibitors Market by Type Outlook

In 2023, the PD-1 segment led the market, capturing a significant 74% of the revenue share. PD-1 inhibitors are effective against various cancers, including melanoma, lung cancer, and bladder cancer, thanks to their ability to produce lasting clinical responses. Their broad applicability and effectiveness have driven widespread adoption, further enhanced by their use in combination with other therapies like chemotherapy and CTLA-4 inhibitors. The market is set for growth due to continuous product innovations and approvals. For example, in February 2023, BeiGene LTD. gained approval from the China National Medical Products Administration (NMPA) for Tislelizumab combined with platinum-based chemotherapy and fluoropyrimidine, a regimen particularly effective for advanced or metastatic gastric cancer patients.

The PD-L1 segment is anticipated to grow the fastest during the forecast period. PD-L1 inhibitors such as Atezolizumab (Tecentriq), Avelumab (Bavencio), and Durvalumab (Imfinzi) are gaining popularity due to their high efficacy. These inhibitors are versatile and can be used alone or in combination for treating various cancers, including non-small cell lung cancer and metastatic Merkel cell carcinoma.

Immune Checkpoint Inhibitors Market by Application Outlook

Lung cancer was the leading application segment in 2023, holding a 26% revenue share. It remains the top cause of cancer-related deaths worldwide, with cases projected to increase from 2.48 million in 2022 to 3.05 million by 2030, according to GLOBOCAN. The high prevalence and mortality rates associated with lung cancer drive the demand for immune checkpoint inhibitors. Recent approvals, such as Merck & Co., Inc.’s KEYTRUDA (pembrolizumab) for stage IB, II, and IIIA non-small cell lung cancer, highlight the critical role of these inhibitors in this segment.

The colorectal cancer segment is expected to see significant growth. Colorectal cancer (CRC) is the third most common cancer globally, affecting about 10% of cancer patients, and is the second leading cause of cancer-related deaths worldwide. The rising incidence of CRC fuels the demand for effective treatments. Merck & Co., Inc.’s KEYTRUDA (pembrolizumab) received FDA approval in June 2020 for treating metastatic colorectal cancer, reflecting ongoing efforts to address this urgent need.

Immune Checkpoint Inhibitors Market by Distribution Channel Outlook

Read More@ Biosimilars Market

Top Manufactures in Immune Checkpoint Inhibitors Market

- Sanofi

- F. Hoffmann-La Roche Ltd.

- Merck & Co.

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Regeneron Pharmaceuticals Inc.

- AstraZeneca PLC

- Shanghai Jhunsi Biosciences Ltd

- Immutep Ltd

- BeiGene Ltd

- GlaxoSmithKline PLC

Immune Checkpoint Inhibitors Market Segmentation:

By Type

- PD-1

- PD-L1

- CTLA-4

- Others

By Application

- Lung Cancer

- Breast Cancer

- Bladder Cancer

- Melanoma

- Cervical Cancer

- Hodgkin Lymphoma

- Colorectal Cancer

- Others

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa (MEA)

Buy this Premium Research Report@ https://www.visionresearchreports.com/report/checkout/39336

You can place an order or ask any questions, please feel free to contact sales@visionresearchreports.com| +1 650-460-3308