by

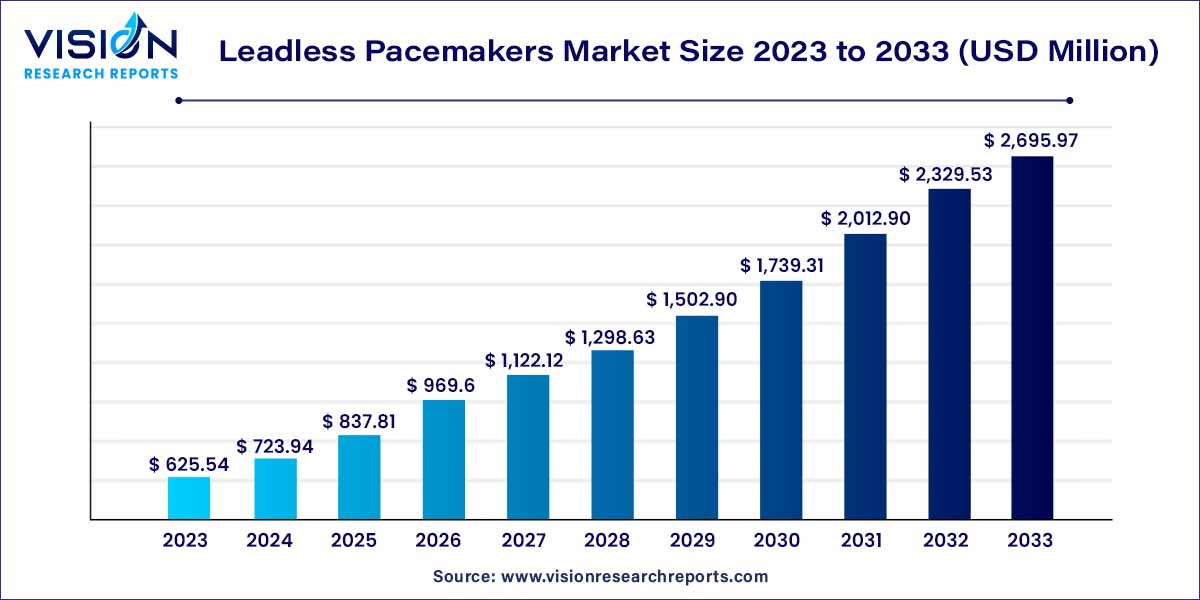

by The global leadless pacemakers market size was estimated at around USD 0.56 billion in 2022 and it is projected to hit around USD 2.42 billion by 2032, growing at a CAGR of 15.74% from 2023 to 2032. The leadless pacemakers market in the United States was accounted for USD 198.8 million in 2022.

Key Pointers

- North America led the global market with the largest market share of 51% in 2022.

- Asia-Pacific is expected to expand at the highest CAGR of 17.07% from 2023 to 2032.

- By Pacing Chamber, the single chamber segment generated the maximum market share of 68% in 2022.

- By Pacing Chamber, the dual chamber segment is anticipated to grow at the noteworthy CAGR of 17.25% between 2023 to 2032.

- By End-use, the hospital segment registered more than 90% of market share in 2022.

- By End-use, the outpatient facilities segment is expected to grow at the fastest CAGR of 16.53% over the forecast period.

The leadless pacemakers market has witnessed remarkable growth and innovation in recent years, revolutionizing the landscape of cardiac healthcare. As a cutting-edge solution for heart rhythm disorders, leadless pacemakers have garnered substantial attention from healthcare providers and patients alike. This overview provides insights into the key aspects shaping the leadless pacemakers market.

Market Growth

The growth of the leadless pacemakers market can be attributed to several key factors. Firstly, the rising prevalence of cardiac arrhythmias and heart-related disorders globally has significantly increased the demand for innovative cardiac pacing solutions. Secondly, advancements in medical technology, particularly in the field of electrophysiology, have led to the development of more efficient and reliable leadless pacemakers. Additionally, the aging population in many countries has contributed to the market expansion, as elderly individuals are more susceptible to heart rhythm disorders. Furthermore, the shift towards minimally invasive procedures in healthcare has boosted the adoption of leadless pacemakers, as these devices offer a safer and more convenient alternative to traditional pacemakers with leads. Lastly, ongoing research and development activities aimed at improving the functionality and durability of leadless pacemakers have bolstered market growth, ensuring a continuous influx of innovative products into the healthcare sector.

Get a Sample: https://www.visionresearchreports.com/report/sample/40884

Report Scope of the Leadless Pacemakers Market

| Report Coverage | Details |

| Revenue Share of North America in 2022 | 51% |

| CAGR of Asia Pacific from 2023 to 2032 | 17.07% |

| Revenue Forecast by 2032 | USD 2.42 billion |

| Growth Rate from 2023 to 2032 | CAGR of 15.74% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Market Analysis (Terms Used) | Value (US$ Million/Billion) or (Volume/Units) |

| Companies Covered | Abbott; Medtronic |

Read More: https://www.heathcareinsights.com/botulinum-toxin-in-urology-market/

Market Dynamics

Drivers

Increasing Prevalence of Cardiac Arrhythmias:

The rising incidence of cardiac arrhythmias and heart-related disorders globally has propelled the demand for advanced cardiac pacing solutions, driving the market for leadless pacemakers.

Minimally Invasive Procedures:

There is a global shift towards minimally invasive medical procedures. Leadless pacemakers, implanted directly into the heart without the need for leads, offer a safer and more convenient alternative to traditional pacemakers. This minimally invasive approach drives their adoption among both patients and healthcare professionals.

Restraints

High Initial Costs:

The initial cost of leadless pacemakers is considerably higher than traditional pacemakers with leads. This cost disparity poses a significant barrier to adoption, particularly in regions with limited healthcare budgets and in healthcare systems heavily reliant on cost-effectiveness.

Limited Expertise and Training:

Implanting leadless pacemakers requires specialized training for healthcare professionals. The lack of expertise in handling these advanced devices can lead to complications during and after the implantation procedure, hindering their widespread adoption.

Opportunities

Remote Monitoring and Data Analytics:

The integration of advanced data analytics with remote monitoring capabilities creates opportunities for personalized patient care. Healthcare providers can analyze real-time data from leadless pacemakers to offer tailored treatment plans, improving patient outcomes and satisfaction.

Focus on MRI Compatibility:

Addressing the limitations related to MRI compatibility can open new avenues for leadless pacemakers. Research and development efforts aimed at ensuring compatibility with MRI scans can broaden the applicability of these devices, especially for patients requiring frequent diagnostic imaging.

Challenges

Battery Replacement Challenges:

While leadless pacemakers have longer battery life compared to traditional pacemakers, replacing the battery still requires a surgical procedure. This replacement process can be complex and costly, impacting the overall cost-effectiveness of leadless pacemakers over the long term.

Regulatory Hurdles:

The regulatory approval process for medical devices is stringent and time-consuming. Delays in obtaining regulatory approvals can significantly impede the market entry of new and advanced leadless pacemakers, limiting choices for healthcare providers and patients.

Pacing Chamber Insights

The single chamber segment dominated the market with a revenue share of 68% in 2022. Single chamber leadless pacemakers are designed to stimulate either the atria or ventricles of the heart. They are compact, self-contained devices that eliminate the need for traditional leads, reducing the risk of lead-related complications. These pacemakers are implanted directly into the heart, ensuring precise and efficient pacing. Single chamber leadless pacemakers are especially suitable for patients with specific heart rhythm disorders, offering a tailored solution that meets their cardiac needs.

The dual chamber segment is expected to grow at the notable CAGR of 17.25% over the forecast period. Dual chamber leadless pacemakers offer more sophisticated pacing options by stimulating both the atria and ventricles of the heart. This dual-chamber functionality allows for synchronized pacing, enhancing the coordination between the heart’s chambers and optimizing cardiac performance. Dual chamber leadless pacemakers are equipped with advanced sensors and algorithms, ensuring accurate detection of the heart’s electrical signals. This precision in pacing is particularly beneficial for patients with complex arrhythmias, as it mimics the heart’s natural rhythm more closely, thereby improving overall cardiac function.

End-use Insights

The hospital segment contributed more than 90% of market share in 2022. Hospitals serve as crucial hubs for cardiac care, where patients with various heart rhythm disorders receive diagnosis, treatment, and follow-up care. In hospitals, leadless pacemakers are deployed in specialized cardiac units, ensuring that patients with conditions such as bradycardia or atrial fibrillation receive prompt and expert care. The integration of these innovative devices within hospital environments not only enhances patient outcomes but also streamlines the overall treatment process.

The outpatient facilities segment is predicted to grow at the fastest CAGR of 16.53% over the forecast period. Outpatient facilities, including specialized cardiology clinics and ambulatory care centers, have become increasingly equipped to handle various cardiac procedures, including leadless pacemaker implantations. These facilities offer a more convenient and patient-friendly environment, allowing individuals to receive necessary cardiac interventions without the need for extended hospital stays. The outpatient approach aligns with the global trend towards minimally invasive procedures, providing patients with advanced cardiac solutions while minimizing disruptions to their daily lives.

Regional Insights

North America led the global market with the largest market share of 51% in 2022. North America stands as a prominent market leader, driven by its advanced healthcare systems, significant investments in research and development, and a high prevalence of cardiac disorders. The region’s robust regulatory framework and early adoption of innovative medical technologies contribute to the widespread use of leadless pacemakers in both the United States and Canada.

Asia-Pacific is expected to witness the fastest CAGR of 17.07% over the forecast period. Asia-Pacific emerges as a rapidly expanding market for leadless pacemakers, driven by increasing healthcare expenditure, rising awareness about advanced cardiac care, and a growing aging population. Countries like China, Japan, and India witness a surge in demand for cardiac devices, including leadless pacemakers, owing to the rising incidence of heart-related disorders. The market in this region is further bolstered by partnerships between international medical device companies and local healthcare providers, enhancing accessibility to innovative cardiac solutions.

Leadless Pacemakers Market Report Segmentations:

By Pacing Chamber

- Single Chamber

- Dual Chamber

By End-use

- Hospitals

- Outpatient Facilities

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Buy this Premium Research Report@ https://www.visionresearchreports.com/report/checkout/40884

You can place an order or ask any questions, please feel free to contact sales@visionresearchreports.com| +1 650-460-3308